Key Takeaways:

- IRS Form 2553 allows eligible businesses to elect S-Corporation tax treatment, which can create tax savings for profitable small business owners.

- An S-Corp is a tax classification, not a separate legal entity, and it changes how the IRS taxes your business at the federal level.

- S-Corp status is often a strong fit for LLC owners, consultants, contractors, and service-based businesses with consistent profits above a reasonable owner salary.

- To qualify for S-Corp election, businesses must meet IRS eligibility rules, including shareholder limits, domestic entity requirements, and single-class stock restrictions.

- Filing Form 2553 accurately and on time is critical, since mistakes involving signatures, effective dates, EINs, or shareholder information can delay or invalidate the election.

- After approval, S-Corps must maintain ongoing compliance through payroll, reasonable compensation, Form 1120-S filings, and proper accounting and recordkeeping practices.

If you’ve ever wondered how some small business owners manage to keep more of what they earn, the answer usually comes down to one thing: how their business is taxed. IRS Form 2553 is the document that lets eligible businesses elect S-Corporation (S-Corp) tax treatment, which is one of the most impactful filings a small business owner can make.

S-Corp elections have become increasingly popular among LLC members and small business owners looking to reduce self-employment taxes and take greater control of their tax obligations. And for good reason: the tax structure you choose affects not just what you owe at the end of the year, but also your payroll requirements, compliance obligations, and long-term financial planning.

If you’ve been unclear about the difference between an LLC and an S-Corp, unsure about who actually qualifies, or worried about making a filing mistake that costs you time and money, this guide is here to help. We’ll review what Form 2553 is and what it actually does, who qualifies for S-Corp status, and how a business tax accountant can guide you toward the right decisions.

USA Tax Gurus is a team of enrolled agents and licensed CPAs who can help you take control of your business finances to maximize profits, reduce taxes, and provide increased financial clarity. We’re QuickBooks Pro Advisors, but our tech-savvy team can work in almost any accounting platform, including Wave, Zoho, and more. Schedule your free consultation today with a member of our team to learn more!

What Is IRS Form 2553?

IRS Form 2553 is the official election form used to request S-Corporation tax treatment under Internal Revenue Code Section 1362. When your qualifying business files this form, you’re telling the IRS that you want to be taxed as an S-Corp rather than under your default tax classification. It’s a relatively straightforward form, but the rules around eligibility, timing, and accuracy mean that you’ll want to be fully informed before you make the change.

Pro Tip: Filing Form 2553 doesn’t create a corporation or an LLC. Your legal business entity stays exactly as it is, and no new entity is formed in the process. What changes is how the IRS treats your business for federal tax purposes.

So, how does S-Corp taxation actually work? Instead of the business itself paying federal income tax, profits and losses pass through to the owners, who then report them on their personal tax returns. This pass-through taxation model helps owners avoid the double taxation that C-Corporations face, where income gets taxed once at the corporate level and again when distributed to shareholders.

Form 2553 is available to LLCs, corporations, and certain other eligible domestic entities that meet IRS requirements. Once the election is approved, the business operates under a specific set of IRS rules governing everything from shareholder limits to stock classes.

What Is an S-Corporation?

An S-Corporation isn’t a legal entity type – it’s a tax classification. When you elect S-Corp status, you’re not changing your business structure at the state level. You’re changing how the IRS taxes your business at the federal level.

It helps to see how S-Corp status compares to other common business entities:

- A sole proprietorship is the simplest setup, but it doesn’t leave much room for tax planning, and owners pay self-employment tax on all net earnings.

- An LLC taxed under its default classification has flexibility going for it, but owners can end up paying higher self-employment taxes on the full share of business profits.

- A C-Corporation faces potential double taxation, where profits get taxed at the corporate level first and then again when distributed to shareholders as dividends.

| Business Structure | How It’s Taxed | Self-Employment / Payroll Taxes | Main Advantages | Potential Drawbacks |

| Sole Proprietorship | Business income is reported directly on the owner’s personal tax return | Owner pays self-employment tax on all net earnings | Simple setup, minimal paperwork, low administrative costs | Limited tax planning opportunities and full exposure to self-employment taxes |

| LLC (Default Taxation) | Pass-through taxation to the owner(s) | Members generally pay self-employment tax on the full share of profits | Flexible management structure and liability protection | Higher self-employment tax exposure for profitable businesses |

| S-Corporation | Pass-through taxation with S-Corp election through IRS Form 2553 | Owners pay payroll taxes on salary only; distributions are generally not subject to self-employment tax | Potential tax savings, pass-through taxation, greater compensation flexibility | Payroll requirements, stricter IRS compliance rules, reasonable salary requirement |

| C-Corporation | Business pays corporate income tax separately from shareholders | Shareholder-employees pay payroll taxes on wages | Easier to attract investors and issue multiple classes of stock | Potential double taxation on corporate profits and shareholder dividends |

The main tax advantage of S-Corp status is how owner compensation is handled. As an S-Corp owner, you can split your income between a salary and distributions, with only the salary portion subject to payroll taxes. This is where the potential for self-employment tax savings arises, and it’s a big reason why profitable small businesses pursue this election.

There’s an important catch, though. The IRS requires shareholder-employees to pay themselves a reasonable salary before taking distributions. Trying to minimize your salary to reduce payroll taxes is a red flag for the IRS and can trigger unwanted scrutiny.

Who Should Consider Electing S-Corp Status?

S-Corp status tends to be a strong fit for small business owners who have moved past the startup phase and are generating consistent profit. This includes:

- Consultants

- Agencies

- Contractors

- Service-based businesses (like law firms and beauty salons) where the owner is actively working in the business

If your business is bringing in more than you need to cover your personal salary, S-Corp election is worth a closer look.

LLC Owners and S-Corp Status

LLC owners with steady, growing profits are among the most common candidates for this election. When your net income starts climbing well above what a reasonable salary would be, the gap between your salary and distributions is where the tax savings live. The higher your profits, the more meaningful those savings can become.

Solopreneurs and S-Corp Status

Self-employed professionals like doctors, designers, coaches, accountants, and real estate professionals also frequently benefit from S-Corp status. They are typically high-earning individuals who are already running lean operations and want a more tax-efficient way to pay themselves. For many of them, the payroll rules that come with S-Corp status are a worthwhile trade-off.

That said, S-Corp status isn’t the right fit for every business. Startups that are reinvesting all of their income, businesses with minimal profit, and companies pursuing venture capital funding may find the restrictions and administrative obligations more trouble than they’re worth. Owners who aren’t prepared to run payroll or take on additional compliance responsibilities should factor that into their decision.

Before making any entity election, you should take a hard look at your annual net income, payroll obligations, administrative costs, and state tax implications. What works well for one business may not work for another, and these decisions have long-term consequences. A business tax professional can help you evaluate whether S-Corp status fits your goals now and down the road.

IRS Eligibility Requirements for S-Corp Election

Before you file Form 2553, you need to confirm that your business actually qualifies for S-Corp status. The IRS has certain criteria, and failing to meet even one of them means your election won’t be approved. Taking the time to review these rules before filing can save you from a rejection and the trouble of starting over.

- Your business must be a domestic entity, meaning it’s organized and operating in the United States. Foreign corporations and internationally based entities don’t qualify for S-Corp election. This rule applies regardless of where your clients or customers are located.

- S-Corps can have no more than 100 shareholders. For most small businesses, this isn’t a limiting factor, but it’s something to keep in mind if you’re planning to bring on multiple investors or partners down the road. Eligible shareholders include U.S. citizens, permanent residents, and certain trusts and estates, but corporations and partnerships can’t hold S-Corp shares.

- An S-Corp can only have one class of stock. This means all shares must have the same rights to distributions and liquidation proceeds. Businesses with multiple stock classes, which is common in venture-backed companies, don’t meet this requirement.

Certain business types are also disqualified from S-Corp election altogether. They include certain financial institutions, insurance companies, and international sales corporations. If your business falls into one of these categories, S-Corp status isn’t an option.

Pro Tip: It’s also important to know that S-Corp status operates at the federal level, and states don’t always follow suit automatically. Some states tax S-Corps differently than the IRS does, and others mandate a separate state-level election. Checking your state’s rules is a key part of the picture before you file.

Step-by-Step Guide to Filing Form 2553

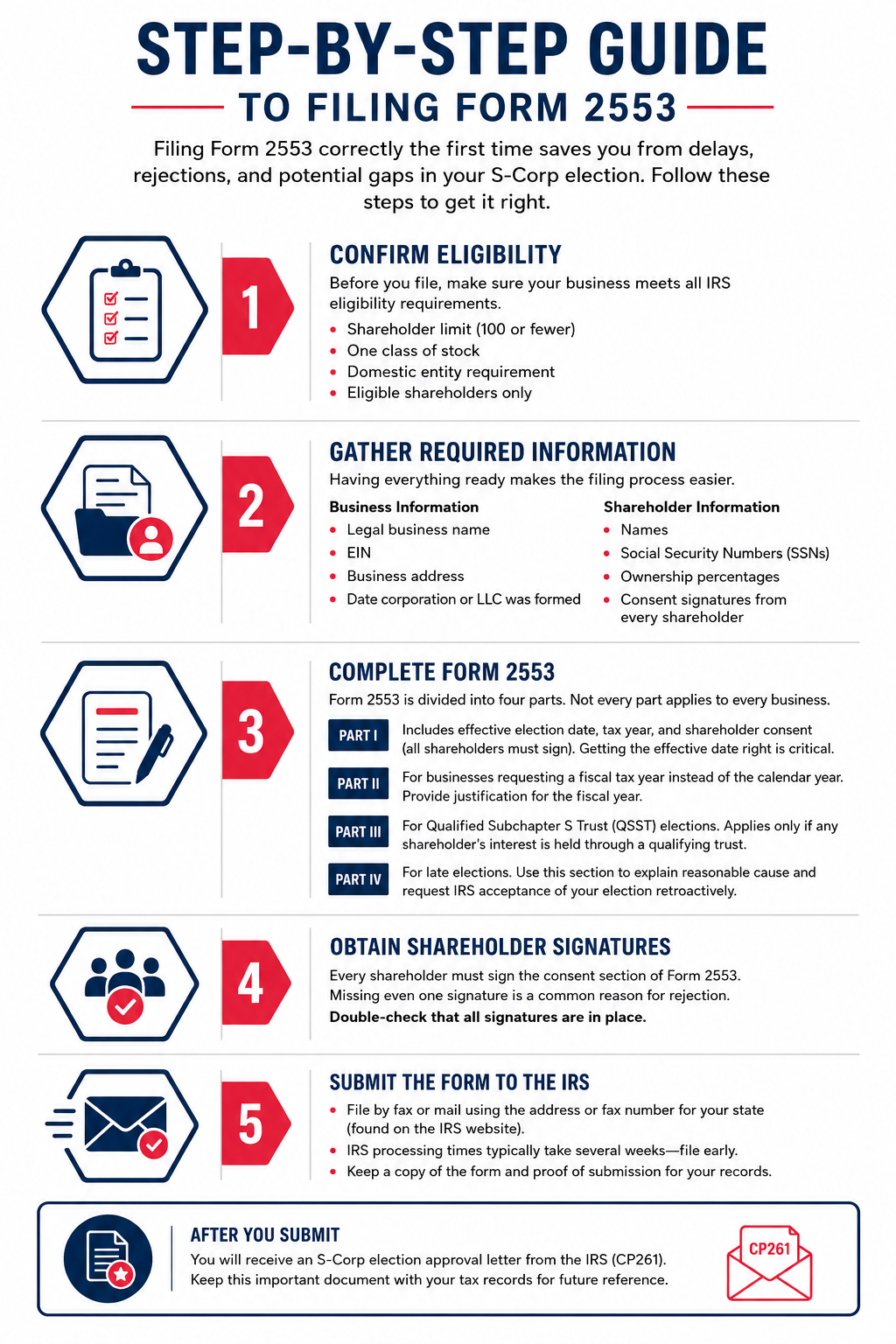

Filing Form 2553 correctly the first time saves you from delays, rejections, and potential gaps in your S-Corp election. The form itself isn’t particularly long, but each section has standards and criteria that you’ll have to confirm that you meet before you submit the form.

Step 1: Confirm Eligibility

Make sure your business meets all IRS eligibility requirements. Review the shareholder limit, stock class rules, and domestic entity prerequisites. If your business doesn’t qualify, there isn’t much point to filing the form.

Step 2: Gather Necessary Information

You’ll need your legal business name, Employer Identification Number (EIN), business address, and the date your corporation or LLC was formed. You’ll also need shareholder information, including names, Social Security Numbers, ownership percentages, and consent signatures from every shareholder.

Step 3: Complete Form 2553

The form is divided into four parts, and not every part applies to every business.

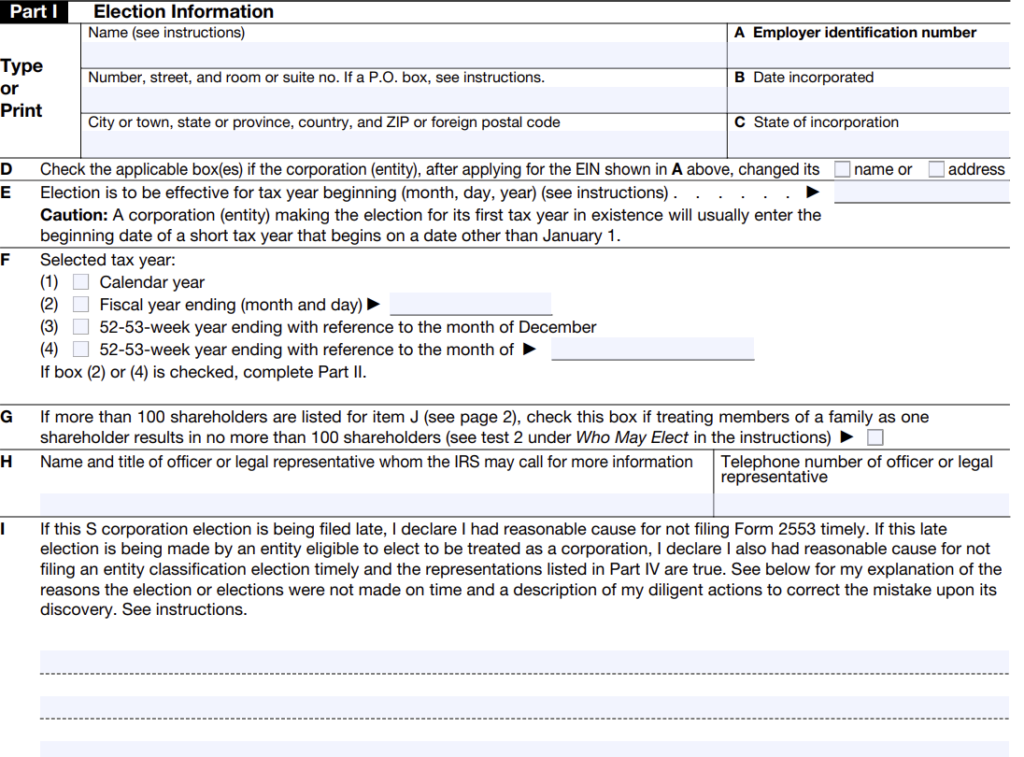

Part I

Part I covers your effective election date, your chosen tax year, and the consent section where all shareholders sign off on the election. Getting the effective date right is particularly important, as errors here can affect when your S-Corp taxation actually begins.

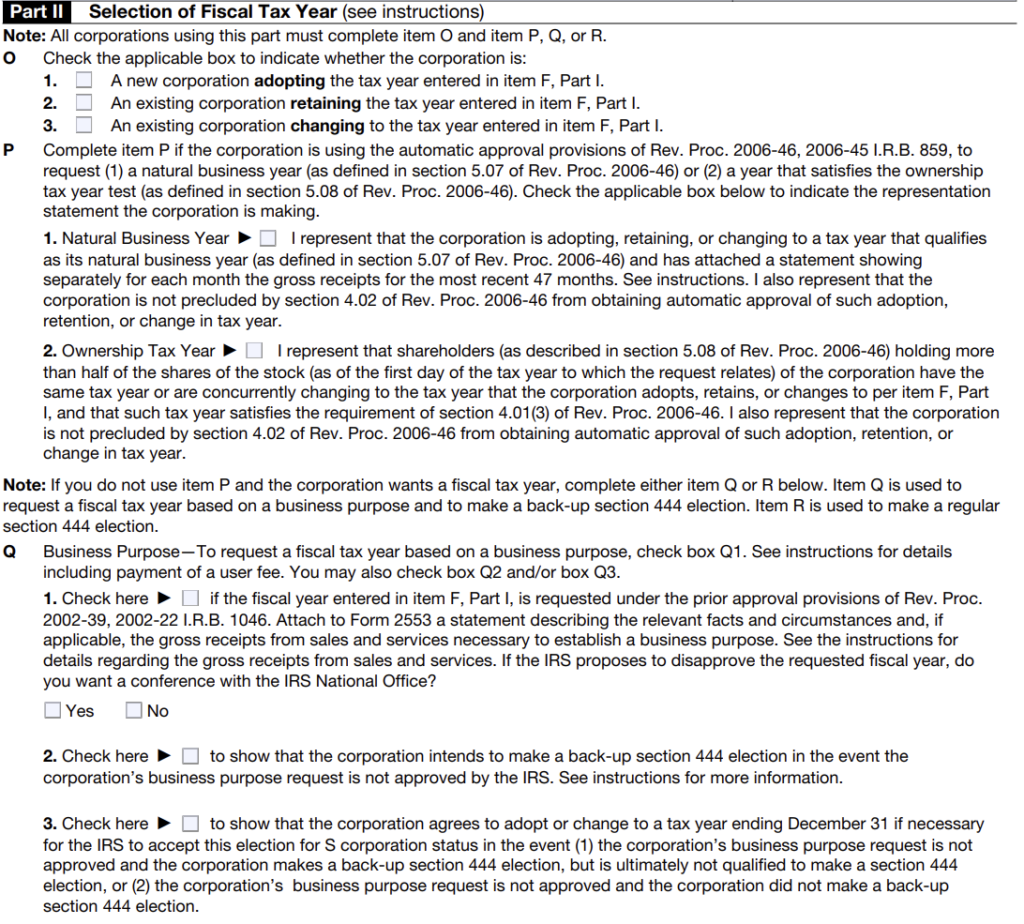

Part II

Part II applies to businesses that want to use a fiscal tax year rather than a calendar year. If you’re requesting a fiscal year that differs from the standard January to December calendar, you’ll need to provide justification here.

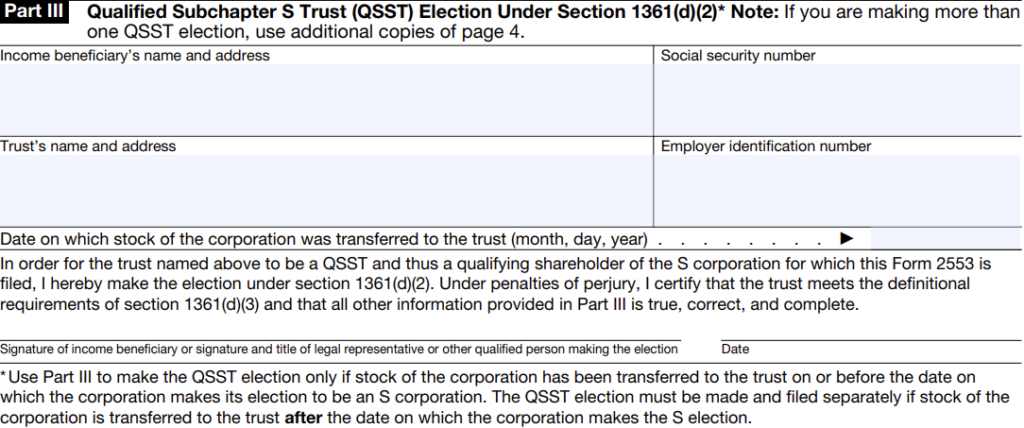

Part III

Part III is for Qualified Subchapter S Trust (QSST) elections. This section only applies if any of your shareholders hold their interest through a qualifying trust.

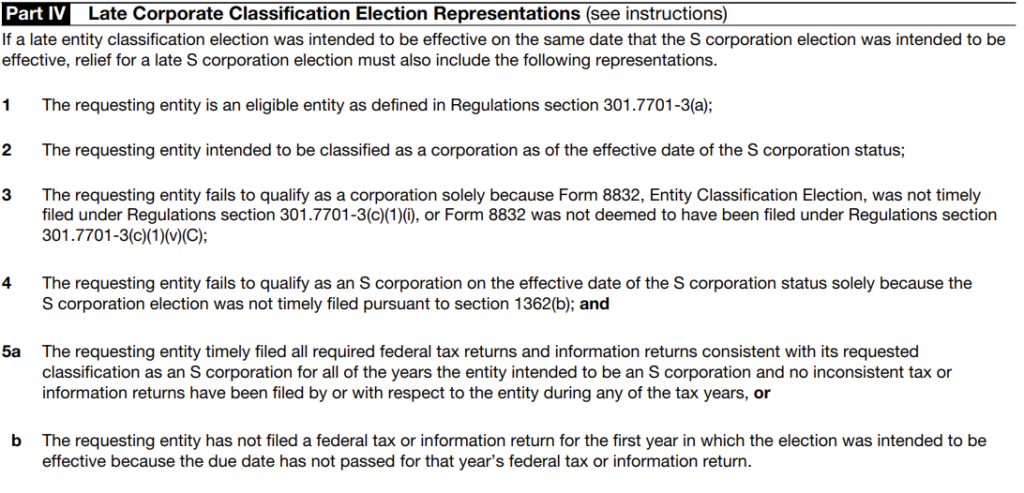

Part IV

Part IV is for businesses filing a late election. If you missed the standard deadline, this section is where you make your case for reasonable cause and request that the IRS accept your election retroactively.

Step 4: Obtain Shareholder Signatures

Every shareholder must sign the consent section of Form 2553. Missing even one signature is one of the most common reasons the IRS rejects elections. Double-check that all signatures are in place before you submit.

Step 5: Submit the Form to the IRS

Form 2553 can be filed by fax or mail, depending on your state and business type. The IRS website provides the correct mailing address and fax number based on your location. Keep in mind that IRS processing times typically run several weeks, so filing early gives you a buffer.

Once you’ve submitted the form, keep a copy for your records along with proof of submission. Your S-Corp election approval letter will be an important document for future tax filings, and having a paper trail protects you if any questions come up later.

Form 2553 Filing Deadlines

Timing is everything when it comes to filing Form 2553. Miss the deadline, and your S-Corp election won’t take effect until the following tax year, potentially costing you an entire year of tax savings.

The standard deadline for filing Form 2553 is two months and 15 days after the beginning of the tax year in which you want the election to take effect. You can also file anytime during the prior tax year if you know in advance that you want S-Corp status for the coming year. For a calendar-year business with a January 1 effective date, that means your deadline falls on March 15.

If you miss the standard deadline, all isn’t lost. The IRS has a late election relief provision that allows businesses to file after the deadline if they can demonstrate reasonable cause for the delay. To qualify, the business must have acted as if it were an S-Corp from the intended effective date, meaning payroll was run, taxes were filed accordingly, and all shareholders were on board. Late election relief isn’t guaranteed, but it’s a legitimate option for businesses that missed the window due to genuine oversights.

Pro Tip: It’s also important to check your state’s deadlines separately. Some states have their own S-Corp election forms, and their deadlines don’t always match the federal timeline. Filing on time with the IRS but missing a state deadline can create complications at the state tax level that are best avoided.

Common Mistakes When Filing Form 2553

Even small errors on Form 2553 can result in a rejection or a delayed election. Knowing where things tend to go wrong makes it easier to get it right the first time.

- Missing Signatures: Every shareholder must sign the consent section of Form 2553, and missing even one signature is among the most common reasons the IRS rejects elections. It sounds like a simple thing to overlook, but it happens regularly, especially in multi-owner businesses where coordinating signatures takes extra effort. Before you submit, do a final check to confirm every signature is in place.

- Incorrect Effective Dates: Some business owners confuse the date of incorporation or LLC formation with the intended effective date of the election. Take the time to confirm the exact date you want S-Corp treatment to start and make sure it’s recorded correctly on the form.

- Filing Before Your EIN Is Issued: Your business must have an Employer Identification Number before you file Form 2553. Filing without one will result in a rejection, and waiting for a new EIN after the fact can push you past the filing deadline. If you’ve recently formed your business and don’t yet have an EIN, apply for one first.

- Using the Wrong Tax Year Information: The tax year you list on Form 2553 must match your entity’s records. A mismatch between what’s on the form and what the IRS has on file for your business can trigger delays or cause your election to be processed incorrectly. Review your existing tax records before completing this section.

- Incomplete Shareholder Data: Missing Social Security Numbers, incorrect ownership percentages, or incomplete shareholder information are all common reasons for rejection. Each shareholder’s information needs to be accurate and complete before the form goes out. Taking a few extra minutes to verify these details can prevent a frustrating back-and-forth with the IRS.

- Forgetting State Compliance: Federal approval of your S-Corp election doesn’t automatically carry over to the state level. Some states want a separate election, and others have their own eligibility rules that differ from the IRS. Assuming your federal approval covers everything is a mistake that can leave you out of compliance at the state level.

- Not Running Payroll Properly: Once your S-Corp election is approved, shareholder-employees have to run payroll and pay themselves a reasonable salary. Skipping this step or delaying payroll setup puts your election at risk and can attract IRS scrutiny. Getting your payroll system in place promptly after approval is an important part of staying compliant.

- Ignoring Reasonable Compensation Rules: The IRS expects S-Corp shareholder-employees to receive a salary that reflects the fair market value of the work they perform. Paying yourself an artificially low salary to reduce payroll taxes is a well-known audit trigger.

What Happens After Filing Form 2553?

Once you’ve submitted Form 2553, the IRS will review your election and send you a confirmation letter known as the CP261 Notice. This letter serves as your official proof that your S-Corp election has been approved, so you’ll want to keep it in a safe place. If you ever need to verify your S-Corp status with a bank, accountant, or state agency, this is the document you’ll need.

After approval, your tax and accounting setup will need to reflect your new status. As an S-Corp, you’re required to run payroll and pay yourself a reasonable salary as a shareholder-employee. You’ll also need to adjust how you handle owner distributions, since those are treated differently from salary for tax purposes and need to be recorded accurately in your books.

Your accounting records will need to be updated to reflect corporate-level filings and shareholder allocations. This is a good time to work with a bookkeeper or CPA who has experience with S-Corp formation and accounting, as the recordkeeping rules are more involved than those for a standard LLC. Getting your books set up correctly from the start saves you time and trouble when tax season arrives.

Pro Tip: S-Corps must file an annual federal tax return using Form 1120-S, which reports the company’s income, deductions, and credits. You’ll also need to keep up with payroll tax filings throughout the year. Staying on top of these rules can keep your S-Corp election in good standing with the IRS.

Questions? Speak to an Experienced S-Corp Accountant

Filing Form 2553 is one of the more consequential decisions a small business owner can make. When it’s done correctly and at the right time, an S-Corp election can open the door to tax savings, a more tax-efficient compensation setup, and improved long-term business planning.

If you’re ready to explore an S-Corp election for your business, connecting with an experienced tax professional can get you started in the right direction. USA Tax Gurus LLC has a team of CPAs, Enrolled Agents, and tax professionals serving clients across 30+ states: we can handle everything from entity elections and payroll setup to ongoing tax planning and compliance. To get started or schedule a consultation, please fill out our contact form or call 213-204-8737 today.

FAQs About IRS Form 2553 and S-Corp Status

How Long Does IRS Approval Take?

IRS processing times for Form 2553 typically run several weeks, though it can take longer during peak filing periods. If you haven’t received a response after 60 days, you can follow up with the IRS directly. Always keep a copy of your submission and any proof of filing in case you need to reference it later.

What Happens if Form 2553 Is Rejected?

If the IRS rejects your Form 2553, you’ll receive a notice explaining the reason. Common rejection reasons include missing signatures, incorrect effective dates, and incomplete shareholder information, all of which can be corrected and resubmitted. Acting quickly after a rejection is important, as delays can push your election into the following tax year.

Is S-Corp Status a Good Fit for Small Businesses?

S-Corp status can be a strong fit for small businesses with consistent, growing profits, but it’s not the right choice for every business. The potential self-employment tax savings need to be weighed against the added costs of payroll, compliance, and accounting. A tax professional can help you evaluate your numbers and determine whether the advantages outweigh the administrative guidelines for your particular situation.

Resources:

- https://www.irs.gov/pub/irs-pdf/f2553.pdf

- https://www.irs.gov/pub/irs-pdf/f1120s.pdf

- https://www.law.cornell.edu/uscode/text/26/1362

- https://www.investopedia.com/terms/c/c-corporation.asp

- https://www.irs.gov/businesses/small-businesses-self-employed/late-election-relief

- https://www.irs.gov/individuals/understanding-your-cp261-notice