Key Takeaways:

- The main difference between CPAs and accountants is that CPAs hold a professional license and may have more insights into tax planning, business strategy, and IRS disputes.

- Accountants commonly handle bookkeeping, payroll, financial reporting, and routine tax preparation for individuals and businesses.

- CPAs can provide additional services such as tax planning, IRS representation, audit services, attestation services, and business advisory support.

- Businesses with straightforward financial needs may be able to operate with basic accounting support, though many owners prefer working with a CPA from the beginning to avoid costly mistakes and uncover tax-saving opportunities.

- Growing companies may benefit from working with a CPA when facing multi-state taxation, financing opportunities, entity changes, business expansion, or other advanced financial considerations.

- Many businesses achieve the best results by working with both an accountant and a CPA, using each professional’s strengths to support different aspects of financial management and long-term planning.

When you need financial guidance for your business, you’ll likely come across two options: an accountant and a Certified Public Accountant (CPA). Although many entrepreneurs or company owners assume these terms describe the same profession, there are important distinctions between the two.

Both accountants and CPAs help individuals and businesses manage financial information, prepare tax returns, and maintain compliant records. However, a CPA has met additional education, examination, experience, and licensing criteria that go beyond those necessary for many accounting positions. Those credentials expand the range of services a CPA can provide while involving more professional responsibilities.

USA Tax Gurus is one of only a handful of online tax and accounting service providers where you have the privilege of getting to work directly with licensed CPAs. We’ll explain the difference between an accountant and a CPA and help you understand how and when your business might benefit from working with a CPA.

USA Tax Gurus is a team of enrolled agents and licensed CPAs who can help you save thousands on taxes. Schedule your free consultation today with a member of our team to learn more!

What Is an Accountant?

An accountant is a financial professional who records, organizes, analyzes, and reports financial information for clients. Their work helps business owners monitor financial performance, maintain accurate records, and meet tax and reporting obligations.

At the most basic level, accountants help ensure that a company’s financial information reflects its actual business activity. This includes tracking revenue, expenses, assets, liabilities, and equity. Their responsibilities can vary depending on their role, education, experience, and the size of the organization they serve: some accountants work internally for a single company, while others provide services through public accounting firms or independent practices.

Common accounting responsibilities include:

- Recording and categorizing financial transactions

- Managing accounts payable and accounts receivable

- Reconciling bank and credit card accounts

- Preparing financial statements

- Assisting with payroll administration

- Monitoring cash flow and operating expenses

- Supporting budgeting and forecasting activities

- Preparing tax returns and tax-related documentation

Many accountants hold bachelor’s degrees in accounting, finance, or related fields. However, the title “accountant” itself is not a licensed designation in the same way as a CPA. In fact, educational backgrounds, certifications, and professional qualifications can vary considerably from one accountant to another.

How Do Business Owners Use Accountants?

Business owners usually work with accountants to manage day-to-day financial operations. For example, a small business may rely on an accountant to maintain its books, generate monthly financial reports, prepare year-end financial statements, and organize records for tax filing purposes.

As a business grows, accounting responsibilities tend to become more involved. Increased transaction volume, payroll obligations, inventory management, and tax requirements can create a greater need for ongoing accounting support. At the same time, there are certain duties and professional authorities that are reserved for licensed CPAs.

What Is a CPA?

A Certified Public Accountant (CPA) is an accountant who has earned a state-issued professional license after meeting rigorous education, examination, and experience guidelines. While CPAs perform many of the same functions as other accounting professionals, the CPA credential reflects a higher level of professional qualification and accountability.

Here’s what you need to know:

- In the United States, CPA licenses are issued and regulated by state boards of accountancy. Although requirements vary slightly by state, candidates must generally complete extensive accounting and business coursework, pass the Uniform CPA Examination, and gain qualifying professional experience before becoming licensed.

- Most states require CPA candidates to complete 150 semester hours of college education, which exceeds the standard 120-credit bachelor’s degree rule. This additional coursework is intended to provide broader knowledge in accounting, taxation, auditing, business law, and related disciplines.

- After meeting educational criteria, candidates must pass the Uniform CPA Examination, which evaluates a candidate’s knowledge in areas like financial reporting, auditing, taxation, regulatory compliance, and professional responsibilities. The examination is widely regarded as one of the most demanding professional licensing exams in the business field.

- CPA candidates must normally complete a designated period of supervised accounting experience before obtaining licensure. This guideline helps ensure that newly licensed CPAs possess practical experience in addition to academic and examination-based knowledge.

- Licensed CPAs must complete continuing professional education (CPE) requirements throughout their careers to maintain their licenses. This helps CPAs remain current on tax law changes, accounting standards, regulatory updates, and professional ethics guidelines.

- Depending on applicable regulations and circumstances, CPAs may perform audits, issue certain attestation reports, represent clients before the Internal Revenue Service, and provide services that call for a licensed accounting professional.

Many lenders, investors, government agencies, and financial institutions give more credibility to financial information prepared, reviewed, or certified by a CPA. As a result, businesses frequently engage CPAs when financial decisions involve outside stakeholders, regulatory requirements, or advanced tax considerations.

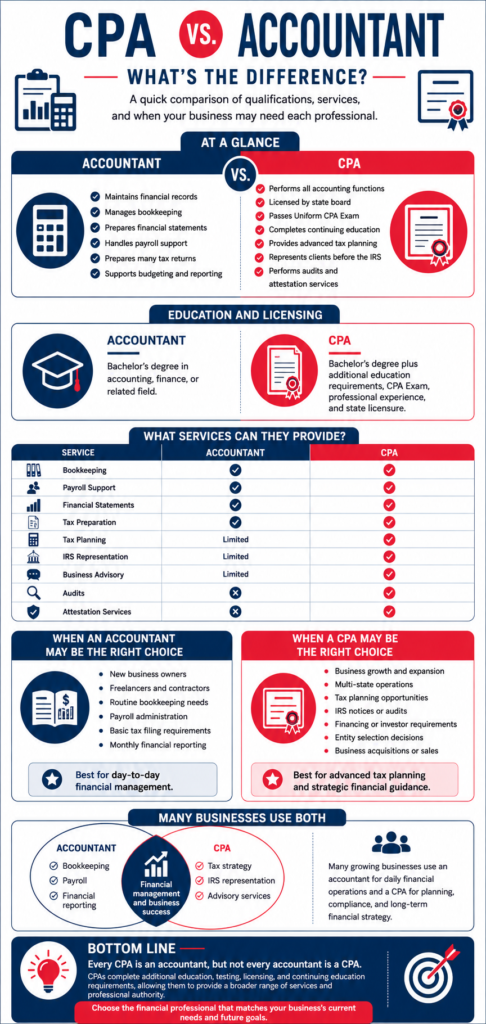

CPAs vs. Accountants: an Overview

| Responsibility | Accountant | CPA |

| Record financial transactions | ✓ | ✓ |

| Maintain bookkeeping records | ✓ | ✓ |

| Prepare financial statements | ✓ | ✓ |

| Manage accounts payable and receivable | ✓ | ✓ |

| Process payroll and payroll reporting | ✓ | ✓ |

| Prepare individual tax returns | ✓ | ✓ |

| Prepare business tax returns | ✓ | ✓ |

| Tax planning and strategy development | Limited depending on experience | ✓ |

| IRS representation for clients | Limited authority depending on credentials | ✓ |

| Financial forecasting and budgeting | ✓ | ✓ |

| Cash flow analysis | ✓ | ✓ |

| Business advisory services | Limited depending on experience | ✓ |

| Entity selection guidance | Limited | ✓ |

| Merger and acquisition support | Limited | ✓ |

| Business valuation services | Limited | ✓ |

| Perform financial statement audits | ✗ | ✓ |

| Issue audit opinions | ✗ | ✓ |

| Conduct attestation services | ✗ | ✓ |

| Meet lender or investor CPA requirements | ✗ | ✓ |

| Subject to state CPA licensing requirements | ✗ | ✓ |

| Continuing professional education requirements | Not generally required | ✓ |

Services Both CPAs and Accountants Can Provide

One reason you may find it hard to distinguish between CPAs and accountants is that the two professions share some responsibilities. Depending on their background and experience, either may help your business with financial management and reporting.

- Bookkeeping and Financial Recordkeeping: Both accountants and CPAs can record transactions, reconcile accounts, organize financial information, and maintain accounting records throughout the year. Proper recordkeeping helps confirm that financial statements, tax filings, and management reports reflect current business activity. When financial information is accurate and current, it becomes easier to evaluate revenue, expenses, and cash flow.

- Financial Statement Preparation: You can hire an accountant or CPA to prepare key financial reports, including income statements, balance sheets, cash flow statements, and other financial summaries. These reports help business owners evaluate operating results and monitor changes over time. Accurate reporting provides insight into the financial position of a business and supports better planning efforts.

- Tax Preparation: Tax preparation is another area where responsibilities frequently overlap. Both accountants and CPAs may prepare individual and business tax returns, calculate tax obligations, gather supporting documentation, and assist clients in meeting filing deadlines. For many small businesses with relatively straightforward tax situations, an accountant may provide all the tax preparation support needed.

- Payroll and Financial Administration: Both accountants and CPAs can assist businesses with payroll administration and related reporting requirements. Their responsibilities may include payroll processing, payroll tax reporting, employee compensation reporting, and year-end tax documentation.

- Budgeting and Financial Analysis: Both professionals may help businesses evaluate financial performance through budgeting and reporting activities. This may include revenue analysis, expense tracking, budget development, cash flow monitoring, and financial performance reviews. These services provide business owners with valuable insight into company operations and financial trends.

When is an Accountant Enough?

For many companies, particularly those in the early stages of growth, an accountant can provide the financial support needed for basic bookkeeping and tax preparation. The key is matching the level of support to the current needs of the business. Many startups, freelancers, independent contractors, and small business owners begin by working with an accountant to establish sound financial practices and then move to a CPA when tax planning, growth decisions, or long-term profitability become priorities.

- Managing Day-to-Day Financial Operations: One of the most common reasons to hire an accountant is to manage daily financial activities. This includes recording transactions, reconciling accounts, tracking expenses, and maintaining accurate books. When these tasks are handled properly, business owners have better insights into their situation.

- Supporting Routine Tax Compliance: An accountant can help prepare tax returns, organize financial records, monitor filing deadlines, and ensure that key documentation is available when needed. This support allows business owners to stay current without dedicating too many internal resources to tax administration.

- Payroll and Administrative Support: As a business begins hiring employees, payroll responsibilities become increasingly important. An accountant can help manage responsibilities like calculating wages, managing tax withholdings, issuing payroll reports, and preparing year-end documentation while helping the business remain compliant.

- Financial Reporting and Performance Monitoring: An accountant can prepare monthly, quarterly, or annual reports that provide insight into the financial condition of the company. These reports help identify trends, evaluate performance, and support business planning efforts.

Many businesses can meet their accounting needs through the support of a qualified accountant. This is particularly true for organizations with relatively straightforward financial operations and limited reporting requirements. Common examples include:

- Freelancers and independent contractors

- Sole proprietorships

- New startups

- Small service-based businesses

- Local retail businesses

- Family-owned companies with uncomplicated accounting needs

When Does a Business Owner Need a CPA?

While many businesses begin with bookkeeping and basic tax preparation, there comes a point where strategic planning becomes increasingly important. A CPA can help evaluate financial decisions before they are made, identify tax-saving opportunities, and provide guidance on issues that affect both current operations and future growth. For many business owners, this transition occurs gradually as the company expands.

Here’s when you may need a CPA:

- Your Business Has a More Involved Tax Situation: Multiple income sources, ownership changes, additional business entities, investments, and interstate operations can all create tax considerations that require careful planning. A CPA can help evaluate how these factors affect tax liability and identify opportunities that may reduce future tax obligations.

- You’re Choosing or Changing a Business Entity: Many business owners begin as sole proprietors or limited liability companies and later consider alternatives such as S corporations or C corporations. A CPA can evaluate how various entity types affect taxation, compensation planning, and future business goals.

- You’re Seeking Financing or Outside Investment: Lenders and investors expect detailed financial information before committing capital. Financial statements, tax returns, cash flow projections, and profitability reports may all be reviewed during the evaluation process. In some situations, outside parties may request financial statements prepared, reviewed, or audited by a CPA.

- You’ve Received an IRS Notice or Are Facing an Audit: While receiving correspondence from the IRS doesn’t automatically indicate a serious problem, you need to respond appropriately. A CPA can review the notice, explain the issues involved, and communicate with tax authorities on your behalf when permitted. They can also help when disputes arise regarding deductions, income reporting, payroll taxes, or business expenses.

- You’re Looking for Tax Planning Instead of Tax Preparation: A CPA can evaluate compensation strategies, retirement contributions, depreciation opportunities, business deductions, and entity elections throughout the year. These planning activities may help reduce tax liability and improve after-tax profitability.

- You’re Planning for Growth, Expansion, or a Business Sale: Opening additional locations, acquiring another company, adding partners, or preparing for a future sale all call for careful financial evaluation. A CPA can help analyze these opportunities and identify potential tax implications before decisions are finalized.

How to Choose the Right Financial Professional

Selecting a financial professional is an important business decision. The right choice for your company depends on several factors, including:

- The size of your business

- The complexity of your financial activities

- Your growth plans

- The level of support you need

An accountant may be sufficient for routine bookkeeping and reporting responsibilities, while a CPA may be a better fit when tax planning, business advisory services, or advanced financial guidance become priorities. But how do you choose the right professional for you?

Evaluate Relevant Experience

Ask about the types of clients they serve and the industries they work with most frequently. Experience with businesses that share your size, ownership structure, and operational model can provide valuable perspective. This background may also help reduce the learning curve associated with becoming familiar with your business.

Review Credentials and Qualifications

While experience is important, credentials may help distinguish one candidate from another when evaluating service providers. If your business needs advanced tax planning, audit services, or representation before tax authorities, professional qualifications absolutely matter.

Consider the Services You Need Today and Tomorrow

Business needs rarely remain static. The accounting support that works well today may not fully address your needs several years from now. For example, a business owner preparing for expansion, seeking financing, or planning to add employees may benefit from working with a professional who can continue providing support as the company grows. Choosing a provider with a broader range of capabilities may help avoid the need to transition to another firm later.

Ask About Technology and Workflow

Modern accounting and tax services rely heavily on technology. Cloud accounting platforms, digital document management systems, secure client portals, and automated reporting tools can improve efficiency and accessibility for both clients and service providers. Understanding how a firm manages information and communicates with clients can help set expectations from the beginning.

Watch for Potential Warning Signs

Not every financial professional will be the right fit for your business. During the evaluation process, potential concerns may include:

- Limited communication or delayed responses

- Lack of experience with businesses similar to yours

- Unclear service descriptions or fee structures

- Minimal attention to tax planning opportunities

- Outdated technology or inefficient workflows

- Difficulty explaining financial concepts in a practical manner

Identifying these issues early can help prevent frustration and misunderstandings later.

A strong professional relationship develops over time. As your financial advisor becomes more familiar with your business, they can provide increasingly valuable insight into your operations, tax considerations, and long-term goals. Taking a thoughtful approach during the selection process can help establish a relationship that supports your business for years to come.

Get CPA-Level Expertise Without CPA-Level Fees

Most business owners would benefit from the expertise of a CPA. The challenge is that many CPA firms charge significantly higher fees than traditional accounting firms. At USA Tax Gurus, we eliminate that tradeoff. Our licensed CPAs provide the tax planning, strategic guidance, and financial expertise of a CPA firm while offering the affordability and responsiveness business owners typically associate with an accountant.

Whether you need tax planning, bookkeeping oversight, business advisory services, entity selection guidance, financial reporting, payroll support, or IRS representation, we provide comprehensive financial solutions designed to help your business grow and succeed.

To get started or schedule a consultation, please fill out our contact form or call 213-204-8737 today.

FAQs About CPAs vs. Accountants

Can an Accountant Become a CPA?

Yes. An accountant can become a CPA by meeting their state’s education, examination, and experience guidelines. This typically includes completing the necessary college coursework, passing the Uniform CPA Examination, gaining qualifying professional experience, and applying for state licensure. Once licensed, the person must also meet ongoing continuing education requirements to maintain the CPA credential

Do CPAs and Accountants Use the Same Accounting Software?

In many cases, yes. Both CPAs and accountants commonly work with accounting platforms such as QuickBooks, Xero, Sage, and other financial management systems. The difference is not usually the software itself but how the financial information is analyzed, interpreted, and applied to tax planning, reporting, and business decision-making.

Is a CPA Required to Prepare Business Taxes?

No. Business tax returns can be prepared by accountants, enrolled agents, tax preparers, and CPAs, depending on the circumstances. However, businesses with multiple owners, multi-state operations, international activities, or advanced tax planning needs may benefit from working with a CPA due to the broader scope of services and qualifications associated with the credential.

Can a CPA Do Bookkeeping?

Yes. CPAs can provide bookkeeping services, financial reporting, payroll support, tax preparation, and advisory services. Many CPA firms offer comprehensive accounting solutions that include both bookkeeping and higher-level tax and financial planning.

Is It Worth Paying More for a CPA?

In many cases, yes. While CPA services may cost more than basic accounting services, proactive tax planning and strategic advice can often generate savings that exceed the additional fees. The value depends on the complexity of your financial situation and the services provided.

How Can You Verify a CPA License?

CPA licenses are issued and regulated by state boards of accountancy. Most state boards maintain online license verification databases that allow the public to confirm whether a CPA’s license is active and in good standing. Reviewing a professional’s license status can provide additional reassurance when selecting a financial advisor.