Key Takeaways:

- IRS Form 5472 is required for U.S. businesses with ≥25% foreign ownership or foreign corporations doing business in the U.S., and it reports transactions with foreign-related parties to prevent tax avoidance.

- You must file one Form 5472 per related foreign party, even if transactions are small or the business had no income.

- The form is filed annually with Form 1120 (or a pro forma 1120 for foreign-owned single-member LLCs) by the standard corporate tax deadline.

- Penalties are severe ($25,000 per form per year), with additional penalties if not corrected promptly.

- Accurate reporting requires detailed records of all transactions (sales, loans, services, etc.) between the U.S. entity and foreign-related parties.

IRS Form 5472 is a reporting requirement for foreign-owned U.S. corporations and U.S. corporations with foreign shareholders holding at least 25% ownership. The IRS uses it to track financial transactions between related parties across international lines, so that income isn’t shifted offshore to avoid U.S. taxes.

Failure to remit this form has consequences. If you either ignore the obligation or file an incomplete return, the IRS imposes a $25,000 penalty per form per tax year, with an additional $25,000 charged if the violation isn’t corrected within 90 days of receiving an IRS notice. These penalties apply even when the business has zero income for the year, which surprises many foreign-owned single-member LLCs.

In this guide, we’ll explain what Form 5472 is, what information it asks for, and how to fill it out correctly. We’ll also cover mistakes that can trigger IRS penalties as well as tips for staying on top of your filing obligations year after year.

USA Tax Gurus is a team of enrolled agents and licensed CPAs who can help you take control of your business finances to maximize profits, reduce taxes, and provide increased financial clarity. We’re QuickBooks Pro Advisors, but our tech-savvy team can work in almost any accounting platform, including Wave, Zoho, and more. Schedule your free consultation today with a member of our team to learn more!

What is IRS Form 5472?

IRS Form 5472, officially titled “Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business,” is a disclosure form used to track financial activity between U.S. businesses and their foreign-related parties. It gives the IRS a clear record of money, property, and services exchanged between a U.S. reporting corporation and the foreign individuals or entities connected to it.

Why Was IRS Form 5472 Developed?

The form is part of the IRS’s efforts to monitor international transactions that could otherwise be used to shift profits out of U.S. tax jurisdiction. Examples include:

- A foreign parent company charging a U.S. subsidiary inflated fees for services.

- A foreign owner making loans to a U.S. entity without proper documentation.

Every reportable transaction between a U.S. reporting corporation and a related foreign party must be disclosed, regardless of whether the amounts seem routine.

When Do You File IRS Form 5472?

Form 5472 is filed annually, attached to either a Form 1120 (U.S. Corporation Income Tax Return) or a pro forma Form 1120, depending on the type of entity filing. The deadline is the same as the filing deadline for the associated income tax return, including any approved extensions.

Pro Tip: You must file a separate Form 5472 for each related party with whom you had reportable transactions during the tax year.

Who Needs to File Form 5472?

Two types of businesses need to file Form 5472:

- U.S. corporations with least one foreign shareholder owning 25% or more of its stock, either directly or indirectly or;

- A foreign corporation engaged in a U.S. trade or business at any point during the tax year.

In both cases, the requirement kicks in as soon as a reportable transaction takes place between the reporting corporation and a related party.

Pro Tip: Even though a single-member LLC is normally treated as a disregarded entity for U.S. tax purposes, the IRS requires it to be treated as a domestic corporation solely for Form 5472 reporting. This means a foreign individual who owns a U.S. LLC must file Form 5472 attached to a pro forma Form 1120, even if the LLC hasn’t earned anything and made no payments during the year, as long as any reportable transaction occurred.

What is a Reportable Transaction for Form 5472?

Reportable transactions include:

- Sales and purchases of goods

- Payments for services

- Rents

- Royalties

- Interest

- Loans

- Advances

- Transfers of property between the reporting corporation and a related party.

Here are three examples of common scenarios that trigger the filing requirement:

- A Chinese national owns 100% of a U.S. single-member LLC that purchases inventory from a Chinese supplier owned by the same individual.

- A U.S. corporation pays management fees to its foreign parent company headquartered in Germany.

- A foreign shareholder loans $50,000 to a U.S. corporation in which they hold a 30% ownership stake.

In each of these cases, a Form 5472 must be filed for the tax year in which the transaction occurred, regardless of the transaction size or the profitability of the business.

Key Terms on IRS Form 5472

Reporting Corporation

A reporting corporation is the U.S. entity responsible for filing Form 5472. It’s either a U.S. corporation with at least 25% foreign ownership or a foreign corporation engaged in a U.S. trade or business. For foreign-owned single-member LLCs, the LLC itself is the reporting corporation, even though it’s otherwise treated as a disregarded entity for federal income tax purposes.

Related Party

A related party is any foreign person or entity connected to the reporting corporation through ownership, control, or a family relationship that meets the IRS definition under IRC Section 267(b) or 707(b)(1). This includes a –

- Foreign parent company

- Foreign shareholder owning 25% or more of the reporting corporation

- Foreign subsidiary and;

- Any entity that shares common ownership with the reporting corporation.

The IRS casts a wide net here. A foreign individual who owns 100% of both the U.S. reporting corporation and a separate foreign company makes that foreign company a related party to the U.S. entity.

Reportable Transaction

A reportable transaction is any exchange of money, property, or services between the reporting corporation and a related party. This includes:

- Sales

- Purchases

- Rents

- Royalties

- Interest payments

- Loans

- Advances

- Contributions

- Distributions

There’s no threshold that exempts a transaction from reporting. A $500 service payment to a related foreign party has the same reporting obligation as a $5 million intercompany loan.

Disregarded Entity

A disregarded entity is a business that the IRS treats as inseparable from its owner for federal income tax purposes. A single-member LLC is the most common example. Under normal tax rules, the LLC’s income and expenses flow directly to the owner’s personal tax return. For Form 5472 purposes, however, a foreign-owned single-member LLC loses its disregarded status and is treated as a corporation.

Foreign Ownership Threshold (The 25% Rule)

A U.S. corporation meets the foreign ownership threshold when a single foreign person owns, directly or indirectly, at least 25% of the corporation’s total voting power or total value of all classes of stock at any point during the tax year. “At any point” is important here. A foreign investor who holds 25% ownership for just one day during the tax year triggers the filing requirement for that entire year.

Constructive Ownership Rules

Constructive ownership rules expand the definition of who “owns” stock for Form 5472 purposes. Under these rules, a person is treated as owning stock held by certain family members, partnerships, corporations, trusts, and estates.

For example, if a foreign individual’s spouse owns 15% of a U.S. corporation and the individual directly owns another 10%, the IRS treats the individual as owning 25%, which satisfies the filing threshold. These rules prevent foreign owners from splitting ownership among family members or related entities to fall below the 25% threshold and avoid the reporting requirement.

When and How to File Form 5472

Form 5472 is due on the same date as the reporting corporation’s income tax return. For a U.S. corporation filing Form 1120, that deadline is April 15th if you’re going by calendar year. For foreign-owned single-member LLCs filing a pro forma Form 1120, the same deadline applies. If the reporting corporation is a foreign corporation filing Form 1120-F, the deadline shifts to June 15th for calendar-year filers.

Pro Tip: If you get an extension for your associated income tax return, it extends the deadline for Form 5472 as well. U.S. corporations can request a six-month extension by filing Form 7004 before the original due date. Please note that an extension gives you more time to file, not more time to pay any taxes owed.

You must attach Form 5472 to the reporting corporation’s Form 1120 or, in the case of a foreign-owned single-member LLC, to a pro forma Form 1120. Both the pro forma Form 1120 and the attached Form 5472 are mailed to the IRS at the address specified in the Form 1120 instructions for foreign-owned entities, which is currently the IRS office in Ogden, Utah.

Can You File IRS Form 5472 Online?

Foreign-owned single-member LLCs filing a pro forma Form 1120 with Form 5472 attached must file a paper form. U.S. corporations that file Form 1120 electronically can include Form 5472 as part of their e-filed return, provided their tax software supports the attachment. If you’re filing multiple Forms 5472 for different related parties, each one must be completed separately and included with the same return.

Information Need to File Form 5472

- Basic Company Details: Before you open Form 5472, you’ll need the reporting corporation’s full legal name, Employer Identification Number (EIN), principal business address, country of incorporation, and the tax year covered by the return. If the reporting corporation is a foreign-owned single-member LLC, the name and EIN on Form 5472 must match exactly what appears on the pro forma Form 1120.

- Foreign Owner Details: You’ll need information for each foreign owner or related party involved in reportable transactions. If the foreign owner is an individual, you’ll need their taxpayer identification number from their home country. For foreign entities, the IRS may require a Foreign Employer Identification Number (FEIN) or the equivalent tax identification number issued by the foreign country.

- Transaction Records Between Related Parties: This includes invoices, contracts, loan agreements, promissory notes, wire transfer records, and bank statements that support each transaction amount entered on the form. The IRS doesn’t require you to attach these documents to Form 5472, but it can request them at any time.

- Financial Data: This includes the amounts you paid and received for sales, purchases, rents, royalties, interest, loans, advances, and any other monetary exchanges with related parties. Each category gets its own line on the form, so you can’t lump transactions together or report a single net figure.

This is when accurate bookkeeping is especially important. Accounting software like QuickBooks, set up with separate transaction categories for related-party activity, makes it easier to pull the figures you need when filing season arrives.

Step-by-Step Guide to Filling Out Form 5472

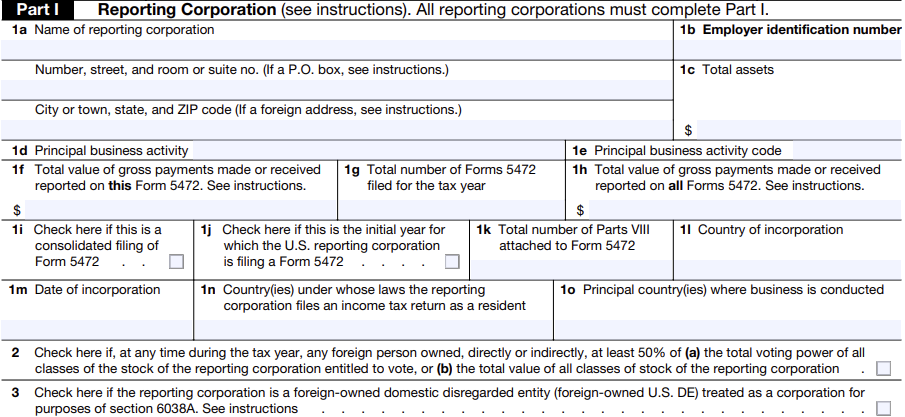

Part I – Reporting Corporation Information

Part I asks for the basic identifying information of the U.S. entity filing the form. You’ll enter the reporting corporation’s legal name, EIN, address, principal business activity, and the country under whose laws the corporation was organized. You’ll also indicate the total percentage of the corporation’s voting stock owned by all foreign shareholders combined, and whether the reporting corporation is a foreign-owned single-member LLC filing a pro forma Form 1120.

- Line 1b asks for the corporation’s principal business activity code, which comes from the same list used on Form 1120. If your LLC imports and resells goods, for example, you’d use a wholesale or retail trade code, not a generic “other” category.

- Line 1c asks for the total number of Forms 5472 filed for the tax year, since a separate form is required for each related party. If your U.S. corporation had reportable transactions with both a foreign parent company and a foreign sibling company, you’d file two separate Forms 5472 and enter “2” on Line 1c of each.

Pro Tip: The most common mistake here is misidentifying the reporting entity. A foreign-owned single-member LLC must list the LLC itself as the reporting corporation, not the foreign owner. The name and EIN entered here must match the pro forma Form 1120 exactly, and the address must be the LLC’s principal place of business, not the foreign owner’s home address.

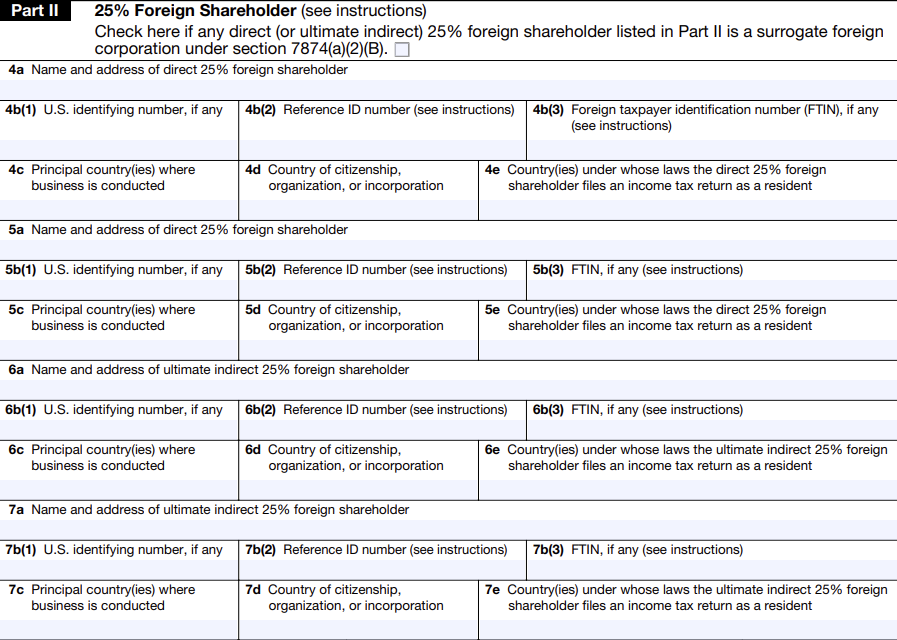

Part II – 25% Foreign Shareholder Information

Part II collects identifying information about each foreign person or entity that owns 25% or more of the reporting corporation, directly or indirectly. You’ll enter the shareholder’s name, address, country of residence or incorporation, U.S. taxpayer identification number (if applicable), foreign taxpayer identification number, and the percentage of ownership held.

Here’s what else you need to know:

- If the 25% shareholder is an individual, you’ll indicate their country of citizenship.

- If the shareholder is a corporation or other entity, you’ll enter the country under whose laws it was created.

- For direct ownership, the percentage entered should reflect the shareholder’s actual ownership stake in the reporting corporation.

- For indirect ownership, the percentage is calculated by multiplying the ownership percentages through each intermediate entity in the chain.

- When there are multiple foreign shareholders who each own 25% or more, each one gets its own Form 5472. If Shareholder A owns 30% and Shareholder B owns 40%, two separate forms are required, one for each shareholder, each attached to the same Form 1120 or pro forma Form 1120.

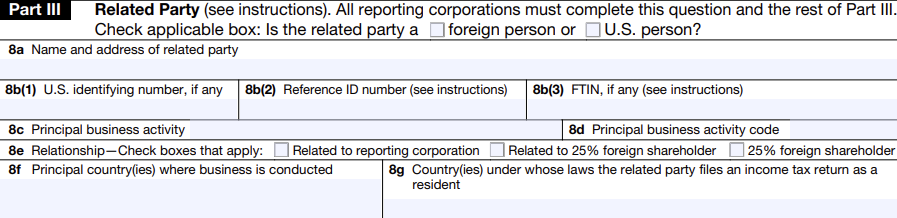

Part III – Related Party Information

Part III identifies the related party with whom the reportable transactions on this particular Form 5472 took place. This might be the 25% foreign shareholder listed in Part II, or it could be a different foreign entity that qualifies as a related party under the IRS rules, such as a foreign company owned by the same shareholder. You’ll enter the related party’s name, address, country of incorporation or residence, and taxpayer identification numbers.

The form asks whether the related party is the same person identified in Part II.

- If your foreign parent company is both the 25% shareholder and the party with whom all transactions occurred, you’d check “yes” and the information carries over.

- If the transactions were with a separate related entity, such as a foreign affiliate that shares common ownership with the reporting corporation, you’d complete Part III with that entity’s information instead.

Direct and indirect relationships are both reportable, but they’re treated differently on the form.

- A direct relationship exists when the related party owns stock in the reporting corporation or vice versa.

- An indirect relationship exists through an intermediary, such as when two companies are both wholly owned by the same foreign individual.

Both types trigger the same reporting requirements, but correctly identifying the nature of the relationship helps ensure the form is completed accurately.

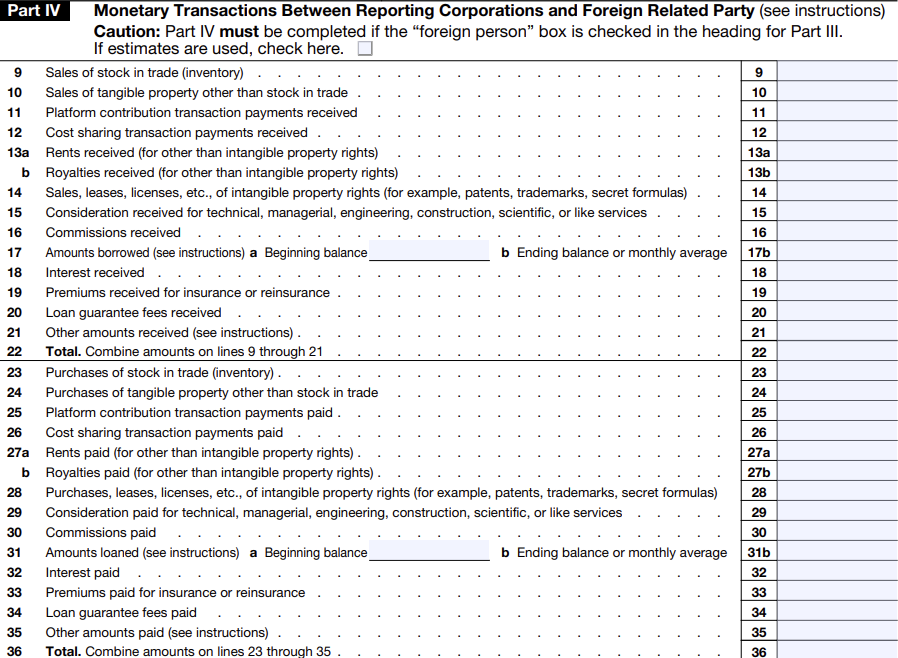

Part IV – Monetary Transactions

Part IV is where you report the dollar amounts of all monetary transactions between the reporting corporation and the related party identified in Part III. The categories covered include:

- Sales of inventory and other property to the related party

- Purchases of inventory and other property from the related party

- Rents and royalties paid to or received from the related party

- Interest paid to the related party on loans or advances

- Interest received from the related party

- Service charges paid to the related party for management fees, technical services, or other services

- Service charges received from the related party

- Loans and advances made to or received from the related party

- Capital contributions made to or received from the related party

- Distributions paid to or received from the related party

Pro Tip: Each line requires the gross amount of the transaction, not the net. If your U.S. corporation paid $30,000 in management fees to its foreign parent and also received $12,000 in interest from that same parent on a loan, both amounts go on their respective lines at full value. Netting them to a single $18,000 figure is incorrect and can result in the form being treated as incomplete.

Part V – Non-Monetary Transactions

Part V covers transactions between the reporting corporation and the related party that didn’t involve a direct cash payment. These include:

- Transfers of property without full payment

- Performance of services without a fee

- The use of property or money without a charge

Even when no money changes hands, the IRS requires these transactions to be reported at their fair market value.

Common examples include:

- A foreign parent company providing rent-free office space to its U.S. subsidiary

- A U.S. corporation transferring intellectual property to a foreign affiliate without receiving compensation

- A related party performing accounting or legal services for the U.S. entity at no charge

Pro Tip: The IRS expects the reported value to reflect what an unrelated third party would have paid for the same property or service under similar conditions, which is the arm’s length standard. If a foreign parent provides software development services to the U.S. entity at no cost, the reported value should reflect the fair market rate for those services, not zero. Entering zero on a non-monetary transaction line when a genuine exchange of value occurred is one of the most common errors on this form.

Part VI – Additional Information

Part VI asks a series of yes-or-no questions about the reporting corporation’s transactions, ownership, and compliance with IRS requirements. These questions cover whether –

- The reporting corporation had any transactions not reported elsewhere on the form;

- It’s a member of a foreign-owned group of corporations and;

- whether transfer pricing documentation was prepared for any of the reported transactions.

Transfer pricing is the practice of setting prices for transactions between related parties. If your U.S. corporation paid its foreign parent $200,000 for services, that price must reflect what an unrelated third party would charge for the same services.

Part VI also includes a section for reporting any additional transactions or disclosures that don’t fit neatly into Parts IV or V. If your reporting corporation had an unusual arrangement with a related party, such as a cost-sharing agreement or a guarantee of a related party’s debt, this is where you’d disclose it.

Common Mistakes When Filing Form 5472

Filing IRS Form 5472 can be confusing, especially for foreign-owned LLCs that may not realize they have reporting obligations in the first place. The rules are strict, the definitions of “reportable transactions” are broader than most expect, and even small mistakes can lead to significant penalties. Understanding the most common filing errors can help you stay compliant, avoid unnecessary fines, and ensure your business is meeting IRS requirements from the start.

Assuming “No Activity” Means No Filing

One of the most common misconceptions is that a foreign-owned LLC with no income or business activity does not need to file. Unfortunately, that’s not the case.

If your LLC is considered a “reporting corporation” (which most foreign-owned single-member LLCs are), you are still required to file Form 5472, even if there was no revenue, expenses, or operations during the year.

Failing to file under this assumption can result in significant penalties, even when the business appears inactive.

Missing Reportable Transactions

Many business owners overlook what the IRS considers a “reportable transaction.” These aren’t limited to large or complex transfers. Routine financial activity can trigger reporting requirements.

Common examples include:

- Funding your LLC’s bank account

- Paying business expenses personally

- Transfers between you and the LLC

- Loans or reimbursements

Even small or one-time transactions must be disclosed. The IRS expects full transparency in any financial relationship between the foreign owner and the U.S. entity.

Filing an Incomplete or Incorrect Form

Accuracy matters just as much as filing itself. Submitting an incomplete or incorrect Form 5472 can be treated the same as not filing at all.

Common errors include:

- Missing or incorrect related party information

- Incorrect ownership percentages

- Failing to properly describe transactions

- Reporting net amounts instead of gross amounts

The IRS requires detailed, transaction-level reporting. Cutting corners or summarizing incorrectly can trigger penalties or additional scrutiny.

Forgetting to File a Separate Form for Each Related Party

Form 5472 is not a one-size-fits-all filing. If your LLC had transactions with multiple related foreign parties, you must file a separate Form 5472 for each one.

For example, if your LLC transacts with both an individual owner and a related foreign company, each relationship requires its own form. Filing only one form in this situation is considered incomplete and can still result in penalties.

Not Attaching Form 5472 to Form 1120 (or Pro Forma 1120)

Form 5472 cannot be filed on its own. It must be submitted alongside Form 1120. For foreign-owned single-member LLCs that are otherwise disregarded entities, this typically means filing a pro forma Form 1120 with Form 5472 attached.

Failing to include Form 5472 with the appropriate return is a common mistake that leads to rejected or noncompliant filings.

Missing the Filing Deadline

Form 5472 follows the same deadline as the associated tax return, which is typically April 15 for calendar-year filers.

While extensions are available, they must be filed before the original due date. Missing the deadline, even unintentionally, can result in automatic penalties, regardless of whether tax is owed.

Assuming DIY Tax Software Covers This

Most standard tax software platforms are not designed to handle Form 5472 requirements, especially for foreign-owned LLCs.

This often leads to:

- Missed filing obligations

- Incorrect or incomplete submissions

- Lack of proper documentation

Because of the complexity and strict compliance requirements, relying solely on DIY tools can be risky. Many foreign owners benefit from working with a tax professional familiar with international reporting rules.

Tips for Staying Compliant with IRS Form 5472

- Keep Detailed Records of All Related-Party Transactions: Every transfer of money, property, or services between your U.S. entity and any related foreign party needs its own paper trail. That means dated invoices, signed contracts, wire transfer confirmations, loan agreements with stated interest rates and repayment terms, and bank statements that match the amounts reported on Form 5472.

- Use Proper Accounting Systems: QuickBooks, Xero, and similar platforms allow you to create custom categories for transactions with specific related parties, so that by the time your filing deadline arrives, the figures for each Form 5472 line item are already organized and totaled.

- Work With Experienced Tax Professionals: A CPA with international tax experience can identify every related party that requires a separate form, confirm that all reportable transactions are captured and categorized correctly, and prepare the pro forma Form 1120 if your entity is a foreign-owned single-member LLC. The cost of professional preparation is a fraction of a single IRS penalty.

Stay Ahead of Form 5472 Compliance With Professional Help

Form 5472 applies to any U.S. corporation with 25% or more foreign ownership and to any foreign-owned single-member LLC that had at least one reportable transaction during the tax year. Every related-party transaction must be reported at its gross amount, categorized correctly, and supported by documentation you can produce if the IRS asks for it.

If you’re a foreign owner of a U.S. entity and you’re not certain whether you’ve been filing Form 5472 correctly, or at all, the right time to find out is now, not after an IRS notice arrives. The team at USA Tax Gurus works with foreign-owned U.S. corporations and single-member LLCs on exactly these obligations. To get started or schedule a consultation, please fill out our contact form or call 213-204-8737 today.